Celsius, a liquidity-strapped crypto lending platform has declared bankruptcy according to a recent court filing from the company’s advisory partner, Kirkland & Ellis.

The crypto lender, which is experiencing a liquidity difficulty, has filed for Chapter 11 bankruptcy protection in the Southern District of New York, according to a statement released by the company late on Wednesday.

The company notified its users through email a few days after the troubled lending platform switched from the law firm Akin Gump Strauss Hauer & Feld LLP it had previously retained to Kirkland & Ellis LLP, the same company that helped Voyager Digital file for bankruptcy last week.

“Today’s filing follows the difficult but necessary decision by Celsius last month to pause withdrawals, swaps and transfers on its platform to stabilize its business and protect its customers. Without a pause, the acceleration of withdrawals would have allowed certain customers – those who were first to act – to be paid in full while leaving others behind to wait for Celsius to harvest value from illiquid or longer-term asset deployment activities before they receive a recovery,” the statement read.

“This is the right decision for our community and company,” said Alex Mashinsky, Celsius’ co-founder and CEO. “We have a strong and experienced team in place to lead Celsius through this process. I am confident that when we look back at the history of Celsius, we will see this as a defining moment, where acting with resolve and confidence served the community and strengthened the future of the company.”

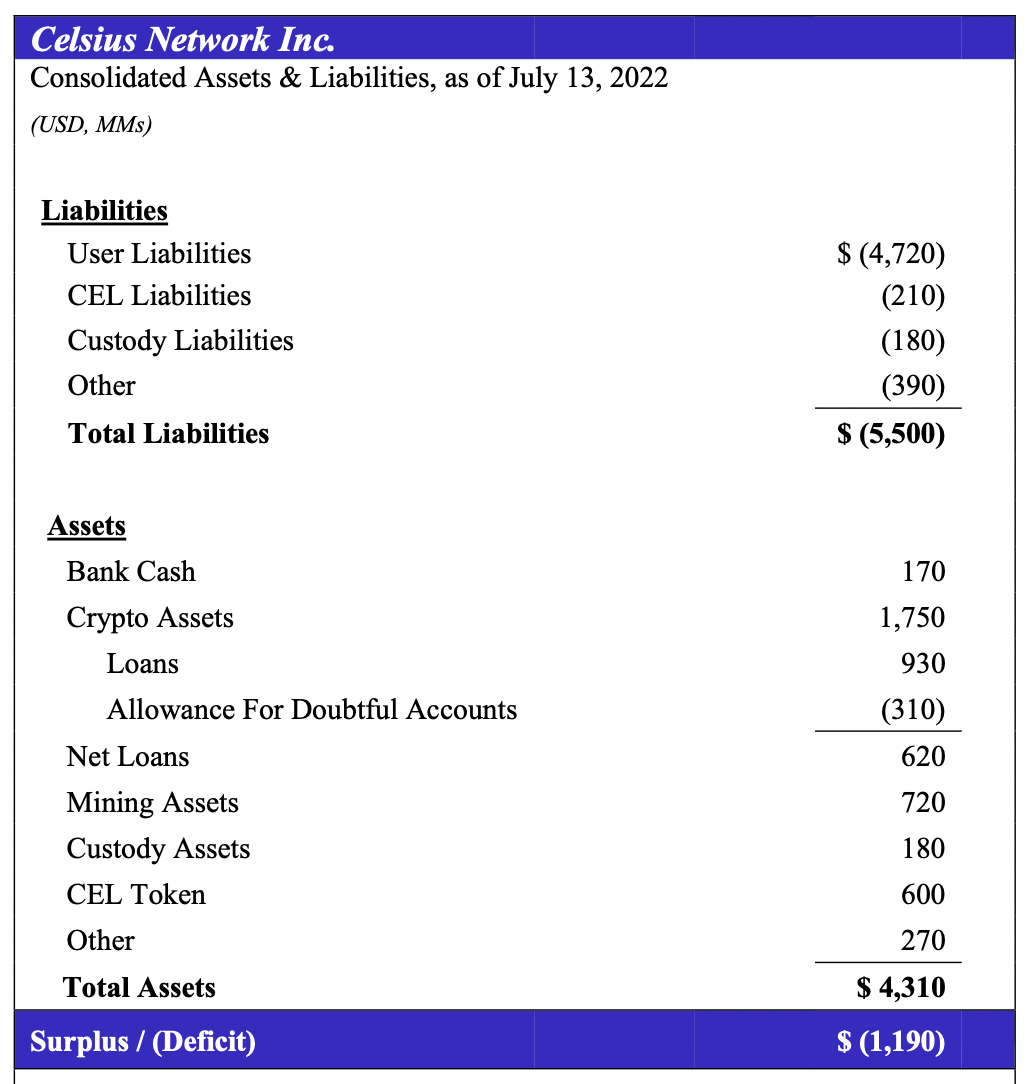

Celsius has assets worth $4.3 billion and liabilities worth $5.5 billion according to the document submitted to the U.S. Bankruptcy Court for the Southern District of New York. Celsius stated that it has roughly $600 million in its CEL coin on its list of assets. The company did point out in the report that CEL’s entire market valuation as of July 12 was approximately $170.3 million.

Celsius wrote off the rest of its decentralized financing (DeFi) debts due to Compound, Aave, and Maker earlier this week, bringing its total debt from its initial $820 million to just $0.013 over the course of a month.

The lender who suspended withdrawals since June 12, cut jobs and hired restructuring experts says it has $167 million in cash on hand, enough to “support certain operations during the restructuring process.”

The company has filed motions with the court to allow it to continue operating “in the normal course,” so that it can pay employees and continue benefits.

The lender that has stopped accepting withdrawals since June 12, made staff reductions, and engaged restructuring specialists claims to have $167 million in cash on hand, which is sufficient to “support certain operations during the restructuring process.”

The company has asked the court to grant permission for it to carry on with its business “in the normal course” in order to pay employees and provide benefits.